{kind=link}

Workers Compensation Insurance Cost in the USA

You just hired your first employee. Congratulations! Workers Compensation Insurance Cost in the USA (2026) Your small business is growing. You have a handshake, a smile, and a brand new employee handbook.

Then reality hits. You remember the law. You need workers’ compensation insurance.

Your heart sinks a little. You have heard horror stories about sky-high premiums. You imagine a massive bill eating into your thin profit margins. You start asking yourself: “Can I afford this? Is this going to break my budget?”

Take a deep breath. You are not alone, and the answer might surprise you.

The workers compensation insurance cost in the USA is not a one-size-fits-all number. It changes based on where you live, what you do, and how safe your workplace is. In 2026, the market is shifting. Some rates are dropping, while others are creeping up.

In this guide, I will walk you through exactly what to expect. We will look at national averages, state-by-state differences, and the hidden factors that drive your final bill. By the end, you will know how to budget for this expense and maybe even lower it.

The Big Picture: National Averages for 2026

Let’s start with the number everyone wants to know: How much does it actually cost?

For most small businesses, the workers compensation insurance cost in the USA averages around $45 per month, or about $542 per year, per employee .

But averages can be misleading. They hide the wide range of what businesses actually pay.

The Range of Possibilities

- Low End: About 23% of small businesses pay less than $30 per month . If you have a low-risk office job and a clean safety record, you might land here.

- Middle Ground: Around 40% of businesses pay between $30 and $60 per month . This is the sweet spot for many contractors, retailers, and service providers.

- High End: Some businesses pay much more. If you work in a high-risk industry like roofing or logging, your costs will be higher.

The 2026 Trend: Mostly Good News

Here is the good news. For most of the country, the workers compensation insurance cost in the USA is staying stable or even going down slightly. Insurers have seen fewer claims over the years thanks to better safety training and automation .

But there are exceptions. Some states are seeing increases. California, for example, just approved an 8.7% pure premium rate increase—its first major hike in over a decade . Washington State also approved a 4.9% average increase for 2026 .

So, while the national picture is calm, you need to look at your own state.

State-by-State Cost Comparison

Where your business is located is one of the biggest factors in your premium. Let’s look at the numbers.

The Lowest Cost States

If you are in one of these states, you are probably paying below the national average. Here are the average monthly costs per employee :

- Ohio: $29

- Texas: $32

- Indiana: $32

- Wisconsin: $33

- Nebraska: $34

The Highest Cost States

On the flip side, some states have significantly higher averages :

- Alabama: $119

- California: $62

- New York: $74

- Louisiana: $71

- Alaska: $64

Why Such a Big Difference?

Why does Alabama have a high average while Texas next door is low? It usually comes down to three things:

- Industry Mix: Some states have more high-risk industries like logging, fishing, or oil drilling. If a state has a lot of dangerous jobs, the average premium goes up .

- Medical Costs: Healthcare prices vary by state. If medical care is expensive in your state, workers’ comp claims cost more, and premiums rise to cover it.

- State Laws: Each state sets its own rules for benefits. States with higher benefit payouts usually have higher premiums .

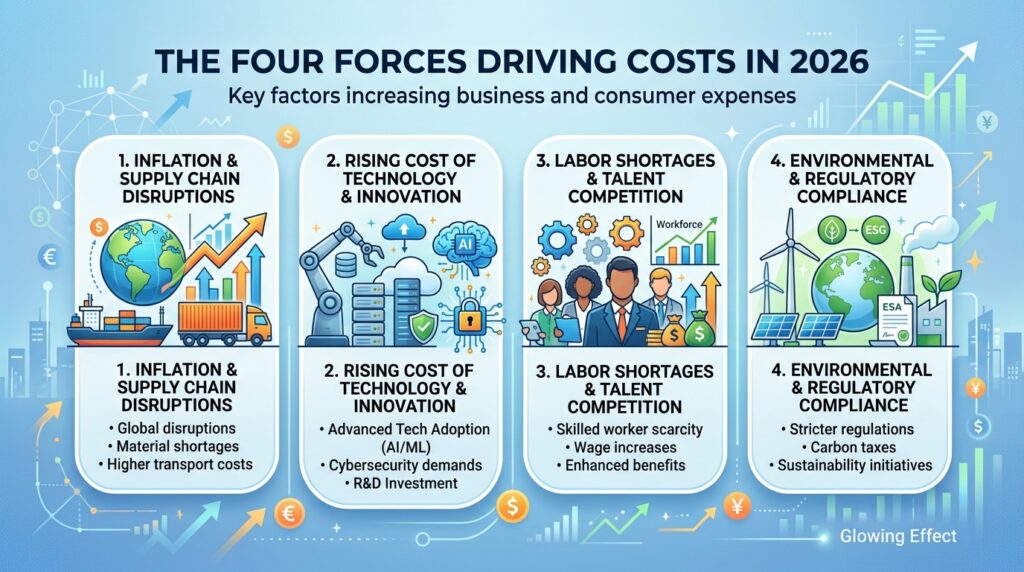

The Four Forces Driving Costs in 2026

The insurance industry is watching four big trends this year. These “forces” are pushing the workers compensation insurance cost in the USA in new directions .

1. Medical Inflation is Back

For years, medical costs were fairly stable. Not anymore. The cost of healthcare is rising again. This directly impacts workers’ comp because the insurance company has to pay those medical bills.

In California, the average cost of a single claim requiring time off work reached nearly $80,000 in 2024 . When claims cost more, premiums eventually follow.

2. Wage Inflation Matters

This one is simple. Workers’ comp benefits replace a portion of an employee’s lost wages. If wages go up, the benefit payments go up.

When a state raises its minimum wage, the cost of claims rises with it. California’s minimum wage is increasing to $16.90 per hour in 2026 . That means if a worker gets hurt, the insurance company pays them more per week. That cost gets passed down to employers through premiums.

3. The “Mega Claim” Problem

Insurers are seeing a rise in “mega claims.” These are severe, expensive cases that cost hundreds of thousands of dollars . They often involve:

- Cumulative trauma: Injuries from repetitive stress over years, not a single accident .

- Litigation: More cases are ending up in court, driven by what experts call “social inflation” and aggressive attorney tactics .

- Older workers: The workforce is aging. Older employees take longer to heal and have more complications, which drives up costs .

4. The “Telelegal” Revolution

This is a weird one. Since the pandemic, many lawyers have gotten comfortable working remotely. This has made it easier for them to take on small workers’ comp cases anywhere in the state .

More lawyers involved means more claims are litigated, and litigation always adds cost.

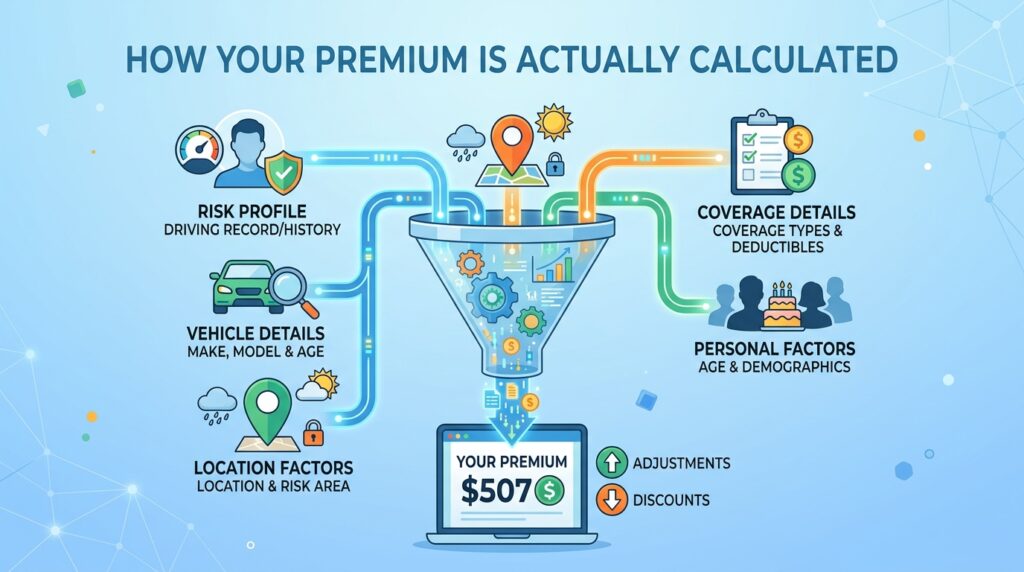

How Your Premium is Actually Calculated

Now that we have covered the averages and trends, let’s look at the math. Insurance companies use a specific formula to calculate your premium.

It looks like this:

(Payroll / 100) x Class Code Rate x Experience Modifier = Base Premium

Let’s break that down.

1. Payroll

The more money you pay your employees, the higher your premium. If you have a $100,000 payroll, your risk is higher than if you have a $50,000 payroll. Simple math.

2. Class Code Rate

Every job type has a “class code.” This is a number that represents the risk of that specific job.

- An office worker (Class Code 8810) has a very low rate, maybe $0.50 per $100 of payroll.

- A roofer (Class Code 5551) has a very high rate, maybe $15.00 or more per $100 of payroll.

You can see actual 2026 rates from state databases. For example, in Missouri, one insurer charges $5.13 per $100 of payroll for Class Code 2070 (likely a moderate-risk job) .

3. Experience Modifier (EMR or “Mod”)

This is your grade. It is a number based on your claims history over the last three to four years .

- 1.0: You are average. You pay the standard rate.

- Below 1.0 (e.g., 0.85): You are better than average. You get a discount.

- Above 1.0 (e.g., 1.2): You are worse than average. You pay a penalty.

This is why safety matters. One bad claim can raise your “mod” and increase your premium for years.

4. Monopolistic States

A quick note. Four states are different: Ohio, North Dakota, Washington, and Wyoming . In these “monopolistic” states, you cannot buy from private insurance companies. You must buy from the state fund.

In Washington, for example, rates are charged per hour worked, not per $100 of payroll. The average rate there is about $1.50 per $100 of payroll after conversion .

Real Examples: What Different Businesses Pay

Let’s put this all together with some real-world examples for 2026.

Example 1: The Low-Risk Consultant

- Business: Marketing Consultant

- Location: Texas

- Employees: 1

- Payroll: $60,000

- Class Code: 8810 (Clerical)

- Experience Mod: 1.0 (New business)

Texas is a low-cost state. The rate for clerical work might be around $0.35 per $100.

Calculation: ($60,000 / 100) x $0.35 = $210 per year. That is about $17.50 per month .

Example 2: The Moderate-Risk Electrician

- Business: Electrical Contractor

- Location: Florida

- Employees: 3

- Payroll: $150,000

- Class Code: 5190 (Electrical Wiring)

- Experience Mod: 1.0

Florida’s rates are moderate. The rate for electricians might be around $3.50 per $100.

Calculation: ($150,000 / 100) x $3.50 = $5,250 per year. That is about $437 per month, or roughly $145 per employee per month.

Example 3: The High-Risk Roofer

- Business: Roofing Company

- Location: California

- Employees: 5

- Payroll: $250,000

- Class Code: 5551 (Roofing)

- Experience Mod: 1.1 (Had one claim last year)

California is a high-cost state, and roofing is a high-risk class. The rate might be $15.00 per $100, and the mod adds a 10% penalty.

Calculation: (($250,000 / 100) x $15.00) x 1.1 = $41,250 per year. That is about $3,437 per month, or $687 per employee per month.

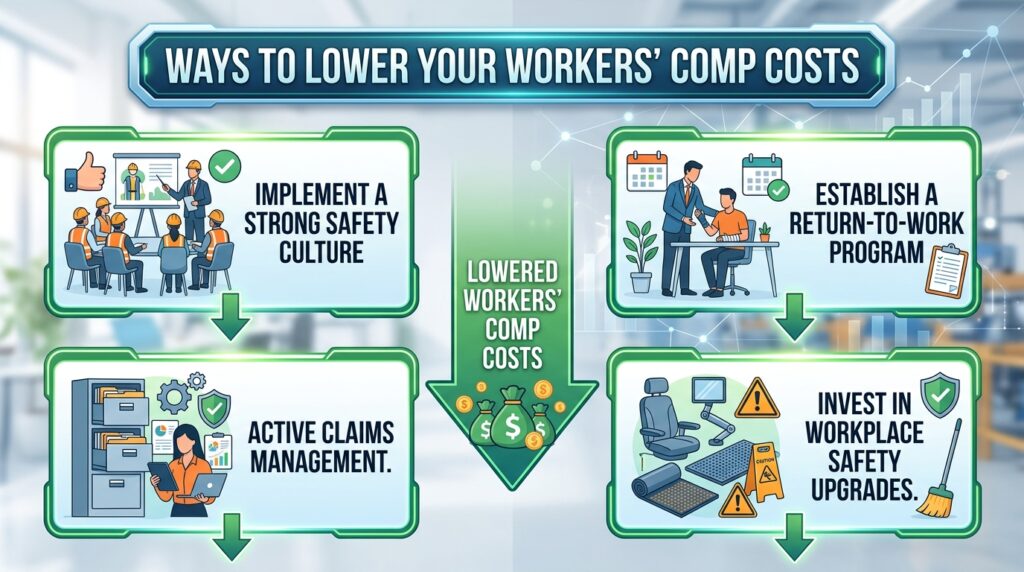

Ways to Lower Your Workers’ Comp Cost

Nobody wants to overpay. Here are five proven strategies to lower your premium in 2026.

1. Create a Safety Program

This is the most effective long-term strategy. Train your employees. Hold safety meetings. Fix hazards immediately.

When you have fewer accidents, your Experience Modifier goes down. In Virginia, the statewide average mod increased from 0.92 to 0.99 recently, showing how claims can impact everyone . You want to be on the good side of that average.

2. Implement a Return-to-Work Program

If an employee gets hurt, do not just send them home. Find light-duty work they can do. Maybe they answer phones while their broken leg heals.

When an employee returns to work quickly, the claim is smaller. A smaller claim has less impact on your future rates .

3. Check Your Class Codes

This is a common mistake. Insurance agents sometimes misclassify employees. If you have an office manager coded as a roofer, you are paying way too much.

Review your class codes every year. Make sure they match what your employees actually do.

4. Consider a Pay-As-You-Go Plan

Traditional policies ask for a big down payment. New “pay-as-you-go” plans sync with your payroll. You pay a little bit each pay period based on actual payroll .

This helps with cash flow. You are not scrambling to find a huge lump sum once a year.

5. Apply for Discounts

In some states, you can get discounts for being claim-free. Washington State, for example, offers a Claim-Free Discount that can lower your base rate by 10% or more . Ask your agent if your state has similar programs.

Frequently Asked Questions

Let’s tackle some common questions about the workers compensation insurance cost in the USA.

I am a sole proprietor with no employees. Do I need coverage?

It depends. If you have no employees, most states do not require you to cover yourself. However, some states let you “opt in” if you want coverage .

If you work alone, you might skip it. But remember: if you get hurt on the job, your health insurance might not cover it, and you cannot get workers’ comp benefits unless you are covered.

My business is in Texas. Do I have to buy it?

Texas is unique. Private employers in Texas are not required to carry workers’ compensation insurance . About 28% of Texas employers opt out.

But be careful. If you opt out and an employee gets hurt, they can sue you. And in a lawsuit, you cannot use the usual legal defenses. You could face unlimited liability .

How often do rates change?

Most states review and adjust rates every year. Insurance companies file new rates with the state, usually effective January 1st . This is why your premium can change even if your payroll stays the same.

What is the difference between workers’ comp and unemployment insurance?

This is a common mix-up.

- Workers’ Compensation: Pays for medical bills and lost wages if an employee gets hurt on the job.

- Unemployment Insurance (SUI): Pays temporary wages if an employee gets laid off.

They are completely different programs with different costs and rules .

What happens if I don’t buy it?

The penalties are severe. Depending on the state, you could face heavy fines, be forced to shut down your business, or even face criminal charges . If an employee gets hurt, you are personally responsible for all their medical bills—which can easily reach six figures.

Conclusion: Budget for It, But Don’t Fear It

The workers compensation insurance cost in the USA in 2026 is manageable for most small businesses. While averages hover around $45 per month, your actual cost depends on your state, your industry, and your safety record.

The market is mostly stable, but watch out for rising medical costs and new regulations, especially if you operate in California or other high-cost states .

Do not think of workers’ comp as just another bill. Think of it as a shield. It protects your employees when they need it most. And it protects your business from financial ruin.

Focus on safety. Keep your workplace clean and your employees trained. Review your class codes. And if you have a claim, manage it carefully to get your employee back to work.

With a little effort, you can keep your premium low and your peace of mind high. Now go out there and grow that business. You have got this.