Let’s talk about something nobody really wants to think about. What happens to the people you love when you’re not around anymore?

It’s a heavy question. But here’s the thing. Answering it now gives you something priceless: peace of mind.

Life insurance is how you protect your family from financial disaster. It means your mortgage gets paid. Your kids can still go to university. Your partner doesn’t have to sell the house.

The problem? Choosing the best life insurance policy in the UK can feel like wading through treacle. There are so many options. So many companies. So much jargon.

I’m here to cut through all that noise. This guide will walk you through exactly how to find the right cover for your family in 2026. No complicated terms. No sales pitch. Just straight-talking advice from someone who’s done the research.For Getting Health insurance click here.

Why You Need Life Insurance (Even If You Think You Don’t)

Here’s a startling fact. According to Legal & General, half of all UK parents don’t have life insurance . That’s millions of families leaving everything to chance.

Think about your life right now. Who depends on you financially?

Maybe you have a partner who works part-time to look after the kids. Maybe you have a mortgage that needs paying every month. Maybe you have little ones who’ll need food, clothes, and school fees for years to come.

If you weren’t here, how would they manage?

That’s what life insurance does. It replaces your income when you can’t be there. It’s not about you. It’s about them.

The good news? It’s probably cheaper than you think. You can get cover starting from under £10 a month . A decent meal out costs more than that.

Understanding the Different Types of Life Insurance

Before you can pick the best life insurance policy, you need to know what’s out there. Let me break it down simply.

Term Life Insurance: Protection for a Set Period

This is the most common type of life cover in the UK. You choose a timeframe – say 20 or 25 years. If you die during that time, the policy pays out. If you outlive it, the cover ends and you get nothing back .

Sounds simple because it is.

Within term insurance, you’ve got a few flavours:

Level Term Insurance: The payout stays the same throughout the policy. If you take out £200,000 cover, that’s what your family gets whether you die in year two or year twenty . This is great for covering things that don’t decrease, like an interest-only mortgage or leaving a lump sum for your family .

Decreasing Term Insurance: The payout goes down over time, usually matching your repayment mortgage. As you pay off your home loan, the potential payout shrinks alongside it . Because the insurer’s risk reduces, these policies are cheaper .

Increasing Term Insurance: The payout rises each year, often in line with inflation. This protects the value of your cover from being eaten away by rising costs. Your premiums will increase too .

Family Income Benefit: Instead of a lump sum, this pays a regular tax-free income to your family until the policy term ends. It’s like replacing your salary month by month .

Whole of Life Insurance: Cover That Never Ends

As the name suggests, this covers you for your entire life. However long you live, the policy guarantees to pay out when you die .

Because a claim is certain, these policies cost much more – sometimes 5 to 15 times more than term insurance .

People usually buy whole of life for:

- Covering funeral costs (the average UK funeral now costs over £4,000)

- Leaving a guaranteed inheritance to children or grandchildren

- Inheritance tax planning, especially if your estate might exceed £325,000

Critical Illness Cover: Protection While You’re Alive

This isn’t life insurance, but it’s often added to life policies. It pays out a lump sum if you’re diagnosed with a serious illness listed in the policy – things like cancer, heart attack, or stroke .

With around 400,000 new cancer cases in the UK every year, this cover can be a lifeline . The money lets you focus on getting better instead of worrying about bills.

Over-50s Life Insurance: Guaranteed Acceptance

Available to people aged 50 to 80, these plans guarantee acceptance without medical questions . They provide a fixed cash sum when you die, often used for funeral expenses.

But be careful. The premiums you pay over time can actually exceed the payout .

Quick Comparison: Which Type Suits You?

How Much Cover Does Your Family Actually Need?

This is where many people get stuck. How much is enough?

Let’s work through it step by step.

1. Add Up Your Debts

Start with what you owe:

- Your mortgage balance

- Any other loans

- Credit card debts

- Car finance

If you weren’t here, would your family cope with these payments? If not, your policy should clear them.

2. Think About Everyday Expenses

What does your family spend each month? Food, utilities, council tax, petrol, activities for the kids.

Multiply that monthly figure by 12, then by the number of years your family would need support. If your youngest is 5 now, you might want cover until they’re 21 or finish university.

3. Factor in Future Costs

University fees. Weddings. Driving lessons. These all cost money. Think about what you’d want to provide for.

4. Don’t Forget Funeral Costs

The average funeral now costs over £4,000 . Including this means your family won’t have to find that money during an already difficult time.

Use a Calculator

Honestly, the easiest way is to use a life insurance calculator. Confused.com has a good one that does the maths for you . It takes about two minutes.

The Top Life Insurance Providers in the UK for 2026

I’ve analysed the market based on claims payout rates, customer service, policy features, and value for money. Here are the providers consistently delivering the best life insurance policy options for UK families.

1. Legal & General: Best for Overall Value and Reliability

Legal & General is the UK’s largest life insurance provider, and for good reason. They combine competitive pricing with exceptional reliability .

Why they stand out:

In 2024, they paid out 97.1% of all life insurance claims, totalling over £890 million . Their policies are straightforward and include terminal illness cover as standard .

Added-value benefits:

Their “Umbrella Benefits” package gives policyholders access to a second medical opinion service and mental health support. Their “Care Concierge” offers telephone advice for family members needing later-life care guidance .

Who it’s for:

Families looking for reliable, no-fuss cover from a market leader at a competitive price .

2. Aviva: Best for Comprehensive Wellness Benefits

Aviva is one of the UK’s most trusted financial services brands, and their 2026 offering is stronger than ever .

Why they stand out:

They paid out an impressive 99.4% of life and critical illness claims in 2024 . Their policies are feature-rich, and their digital health support is market-leading.

Added-value benefits:

The Aviva DigiCare+ app is genuinely useful. It includes:

- 24/7 access to a UK-based GP

- Nutritionist consultations

- Mental health support and therapy sessions

- Annual home health check for 20 different markers

Who it’s for:

Families who want comprehensive digital health and wellbeing support alongside their life cover .

3. Royal London: Best for Ethical, Customer-Focused Cover

As the UK’s largest mutual life insurer, Royal London is owned by its members, not shareholders. This shapes everything they do .

Why they stand out:

Their mutual status means profits are reinvested to improve products and service. They paid 99.4% of all protection claims in 2024 . Their underwriting can be more flexible than some competitors.

Added-value benefits:

Their “Helping Hand” service provides access to dedicated nurses, practical and emotional support, and second medical opinions. It’s real human support, not just a digital add-on .

Who it’s for:

People who value an ethical, customer-owned business and want human-centric support built into their policy .

4. Vitality: Best for Active Families Who Want Rewards

Vitality transformed the market by linking premiums and rewards to healthy living .

Why they stand out:

You earn rewards by tracking physical activity through wearable tech. Hit your targets and you unlock free cinema tickets, coffee shop discounts, and savings on Apple Watches, gym memberships, and flights. For active people, this can dramatically reduce your effective premium . They boast a 99.7% payout rate for life claims (2024) .

Added-value benefits:

The entire Vitality programme is an added benefit. The core offering includes activity tracking rewards, potential premium reductions at renewal for maintaining healthy status, and health screenings .

Who it’s for:

Motivated, active families who want to be rewarded for their healthy lifestyle .

5. Aviva Protection (formerly AIG Life): Best for Complex Health Needs

Following AIG’s acquisition by Aviva in 2024 and rebrand in 2025, this provider maintains its legacy of flexible, adaptable cover .

Why they stand out:

They offer broad acceptance criteria, making them a strong choice for people with complex health histories . They pioneered the inclusion of a ‘Best Doctors’ service and offer ‘Smart Health’ with 24/7 UK-based GP access .

Added-value benefits:

Smart Health provides 24/7 digital GP, fitness plans, and wellness services .

Who it’s for:

Families where someone has complex health needs or requires a more flexible underwriting approach .

6. HSBC Life: Best for Rock-Bottom Premiums

Based on price alone, HSBC Life comes out joint first in Forbes Advisor’s 2026 analysis at just £6.68 per month for a healthy 30-year-old .

Why they stand out:

Their low premiums don’t skimp on features. The policy includes terminal illness cover and a funeral pledge paying up to £5,000 directly to the funeral director if there’s a delay in the main payout . In 2024, HSBC paid out 97.6% of its life insurance claims .

Added-value benefits:

Funeral pledge and terminal illness cover as standard.

Who it’s for:

Budget-conscious families looking for the lowest possible premiums from a trusted high-street name.

7. Beagle Street: Best for High Payout Rates

Beagle Street quoted £7.24 per month in Forbes Advisor’s analysis and boasts one of the highest payout rates in the industry .

Why they stand out:

They paid out 99.8% of claims in 2024 – joint highest in the market . The policy includes terminal illness cover and a £5,000 funeral pledge for delayed payouts.

Added-value benefits:

Excellent claims record and funeral pledge.

Who it’s for:

Families who prioritise the certainty that their claim will be paid above all else.

Quick Comparison Table: Top UK Life Insurance Providers 2026

| Provider | Monthly Premium (30-year-old, £100k cover) | Claims Payout Rate | Best For… |

|---|---|---|---|

| HSBC Life | £6.68 | 97.6% | Lowest premiums |

| Legal & General | £6.68 | 97.1% | Overall value and reliability |

| Quotemehappy.com (Aviva) | £7.09 | 98.8% | High claims payouts |

| Beagle Street | £7.24 | 99.8% | Near-guaranteed claims payment |

| Vitality | £7.90 | 99.7% | Rewards for healthy living |

| Royal London | £8.82 | 99.4% | Ethical, member-focused cover |

| LV= | £9.26 | 97% | Friendly service (for those prioritising this) |

*Note: Premiums are illustrative for a healthy, non-smoking 30-year-old for £100,000 level term cover over 25 years. Your actual quote will vary .*

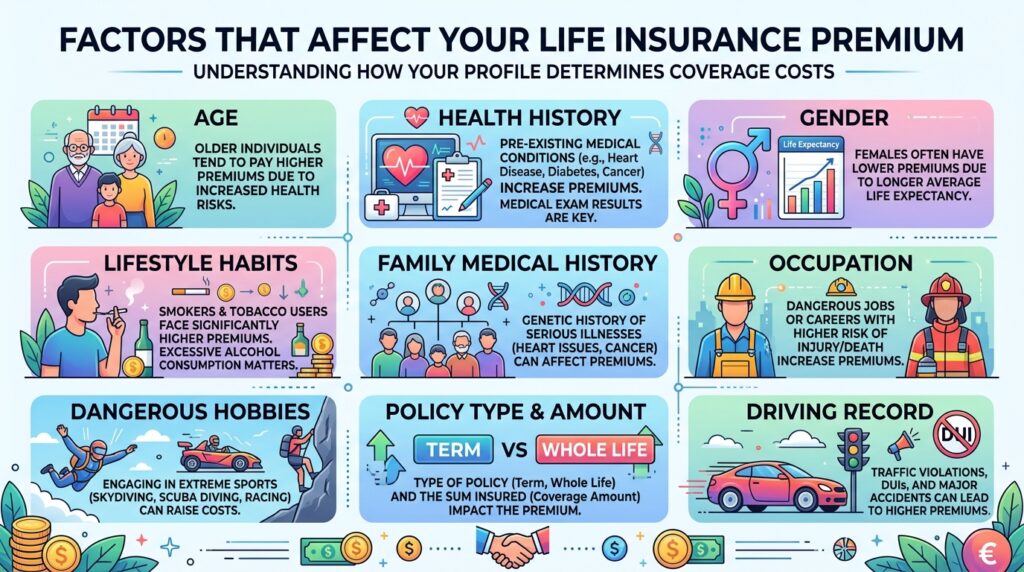

Factors That Affect Your Life Insurance Premium

Your premium isn’t random. Insurers calculate it based on risk. Here’s what they look at.

1. Your Age

This is the biggest factor. The younger you are when you apply, the cheaper your premiums .

Look at the difference. A 25-year-old might pay £4.90 a month for £100,000 of level term cover. A 55-year-old could pay £46.80 for the same policy . That’s nearly ten times more.

The message is clear. Don’t wait. The best time to buy life insurance was yesterday. The next best time is today .

2. Your Health

Insurers ask about your height, weight (BMI), blood pressure, and cholesterol. They also want to know about pre-existing conditions like diabetes, heart disease, or cancer .

Having a medical condition doesn’t mean you can’t get cover. It just makes it more important to use a broker who knows which insurers offer the best terms for your situation .

3. Smoking and Vaping

This is the single biggest lifestyle factor. Smokers can pay double or even triple what non-smokers pay .

A 35-year-old non-smoker might pay £15.40 for £250,000 cover. A smoker of the same age could pay £29.30 .

To be classed as a non-smoker, you need to have been nicotine-free for at least 12 months. This includes vapes, patches, and gum .

4. Family Medical History

If close relatives (parents or siblings) had hereditary conditions like heart disease, stroke, or certain cancers before age 60 or 65, this can affect your premium .

5. Your Job and Hobbies

Dangerous jobs (working at heights, with hazardous materials) or risky hobbies (mountaineering, private piloting, motorsports) can increase your costs .

6. The Policy Itself

- Type of cover: Decreasing term is cheaper than level term. Adding critical illness increases the cost .

- Amount of cover: More cover means higher premiums. Calculate what you actually need .

- Length of term: A 30-year policy costs more than a 20-year policy for the same amount .

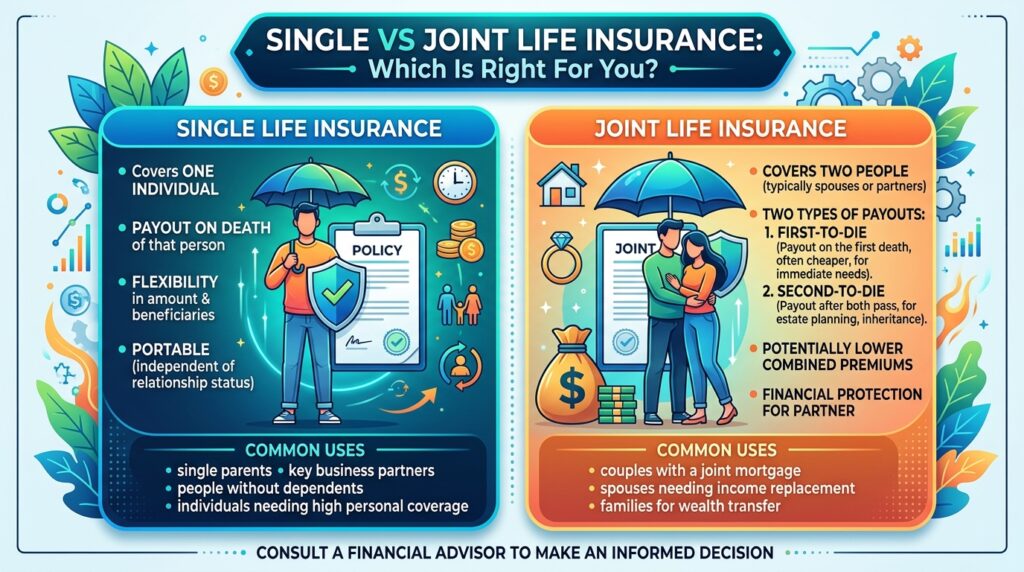

Single vs Joint Life Insurance: Which Is Right for You?

If you’re in a couple, you have a choice.

Joint life insurance covers two people under one policy. It pays out once, on the first death. It’s usually cheaper than two separate policies .

Single life insurance covers one person. You can each take out your own policy. If both policies pay out (for example, if you both pass away), your beneficiaries receive both payouts .

Which is better? It depends.

If both partners contribute to household finances, two single policies might make sense. That way, if one dies, the survivor still has their own cover in place. If you’d bought joint cover, the surviving partner would need to apply for new insurance later, at an older age and potentially with health issues .

Should You Put Your Life Insurance in Trust?

This is one of those technical things that can save your family thousands. Yet most people never hear about it.

Putting your policy “in trust” means it doesn’t form part of your estate when you die. Here’s why that matters.

If your estate (including your life insurance payout) is worth more than £325,000, your beneficiaries pay 40% inheritance tax on everything above that threshold .

A £300,000 payout plus a house worth £300,000 equals a £600,000 estate. That’s £275,000 over the threshold. At 40% tax, your family loses £110,000 to HMRC.

Put the policy in trust and it’s outside your estate. Your family gets the full amount, tax-free .

Trusts also usually mean faster payouts because they don’t have to go through probate .

Most insurers can help you set this up when you apply. It takes five minutes and costs nothing. Do it.

How to Get the Best Life Insurance Policy for Your Family

Follow these steps to find the right cover at the right price.

1. Work Out What You Need

Use the calculation method I shared earlier. Add up debts, multiply monthly expenses by years of support, and include future costs and funeral expenses .

2. Choose the Right Type of Policy

Match the policy to what you’re protecting:

- Repayment mortgage → Decreasing term

- Family protection → Level term or family income benefit

- Inheritance or funeral costs → Whole of life

3. Compare Quotes from Multiple Providers

Don’t just accept the first quote you see. Use comparison sites or a broker to see what’s available. Prices vary wildly between insurers for the same cover .

4. Be Honest on Your Application

This is crucial. If you hide something – smoking, health conditions, risky hobbies – and the insurer finds out later, they can refuse to pay your claim. Your family loses everything .

5. Put Your Policy in Trust

Ask your insurer to put the policy in trust. It takes minutes and saves your family from inheritance tax .

6. Review Your Cover Regularly

Life changes. You might have more children, move house, or pay off your mortgage. Review your cover every few years to make sure it still fits .

Frequently Asked Questions About Life Insurance in the UK

Q: How much does life insurance cost per month?

A: It depends on your age, health, and the cover you choose. A healthy 25-year-old might pay less than £5 a month for £100,000 of level term cover. A 55-year-old could pay over £45 for the same policy . Smokers pay significantly more.

Q: What’s the best life insurance policy for a family?

A: For most families, a level term policy providing a lump sum is a solid choice. It gives flexibility to clear debts and provide ongoing support. Legal & General and Aviva are strong contenders .

Q: Do I need life insurance if I have death in service through work?

A: Death in service is valuable, but it usually ends if you change jobs. Having your own policy gives you cover you control, regardless of where you work .

Q: Can I get life insurance with a pre-existing medical condition?

A: Yes. Having a condition like diabetes or heart disease doesn’t mean you can’t get cover. It may cost more, and you might need to use a specialist broker who knows which insurers offer the best terms for your specific condition .

Q: Will my family pay tax on the life insurance payout?

A: They will if the total value of your estate (including the payout) exceeds £325,000. You can avoid this by putting your policy in trust, which separates it from your estate .

Q: Is critical illness cover worth it?

A: For many families, yes. If you become seriously ill and can’t work, a critical illness payout can be a financial lifeline. It covers mortgage payments, bills, and gives you space to focus on recovery .

Q: What’s the difference between term and whole of life insurance?

A: Term insurance covers you for a set period (like 20 years) and pays out only if you die during that time. Whole of life covers you forever and guarantees a payout whenever you die, but costs much more .

Q: Can my children inherit the life insurance money?

A: Yes, but if they’re under 18, you need to nominate a trustee to look after the money until they come of age. Putting the policy in trust is the best way to ensure your children receive the money exactly as you intend .

Q: When should I buy life insurance?

A: The best time is when you have people who depend on you financially. For many, that’s when they buy a house, have children, or get married. But from a cost perspective, the younger you are when you buy, the cheaper it is .

Q: What happens if I outlive my term life insurance policy?

A: The cover ends and you receive nothing back. That’s by design – term insurance is pure protection, not an investment. If you still need cover at that point, you’d need to take out a new policy .

Conclusion: Your Family Deserves the Best Life Insurance Policy

Choosing life insurance isn’t about you. It’s about the people you love.

It’s about knowing your mortgage will be paid. Your children can stay in their school. Your partner won’t have to sell the family home.

The best life insurance policy is the one that fits your family’s needs, your budget, and gives you genuine peace of mind.

Start by working out what you need to protect. Use the figures I shared – add up debts, multiply monthly expenses, include future costs and funeral expenses .

Then choose the right type. For most families, a level term policy from a reliable provider like Legal & General or Aviva hits the sweet spot between cost and cover .

Compare quotes from multiple providers. Be honest about your health and lifestyle. And please, put your policy in trust. It costs nothing and saves your family from a massive tax bill .

The average cost of getting this wrong? Your family’s financial security. The cost of getting it right? A few pounds a month.

Don’t put it off. The best time to protect your family is now.