So, you’re ready to take your business to the next level. You need a business credit card to manage expenses, build credit, and keep your personal money separate from your company’s cash. But there is one big problem staring you right in the face on every application: Social Security Number (SSN) .

If you don’t have an SSN—maybe you’re a non-resident, an immigrant entrepreneur, or an international business owner—that little box on the application can feel like a locked door. You might be thinking, “I guess I just can’t get one.”

Stop right there. That is simply not true. Learning how to get a business credit card without an SSN is a skill that thousands of international entrepreneurs master every year.For car loan information click here.

Getting a business credit card with no SSN is absolutely possible. You just need to know the right path to take. In fact, a whole new world of financial technology companies (fintech) and traditional banks are waking up to the fact that global citizens and immigrants need access to credit. Understanding how to get a business credit card in this specific situation is all about knowing which doors to knock on.

In this guide, I’m going to walk you through exactly how to get a business credit card when you don’t have that nine-digit number. We’ll cover what you need instead of an SSN, which companies are friendly to non-SSN holders, and the step-by-step process to get that plastic (or metal) in your wallet. By the end, you will know exactly how to get a business credit card that works for your unique situation.

Why Do Credit Cards Ask for an SSN Anyway?

Before we figure out how to get a business credit card without one, let’s understand why the SSN is there in the first place. It’s not just to annoy you.

Banks and card issuers are in the business of lending money. Before they hand you a piece of plastic with a $10,000 limit, they want to know you’re good for it. In the United States, the primary way they check your reliability is by looking at your personal credit history .

Your SSN is the key that unlocks that credit report. It tells the bank:

- Have you paid back loans on time?

- Do you carry a lot of debt?

- Have you ever declared bankruptcy?

For most small business cards, the bank also requires a personal guarantee. This is a fancy way of saying, “If your business goes under and can’t pay the bill, you are personally on the hook for it.” Because of this personal risk, they absolutely want to check your personal credit, which usually requires an SSN or an alternative ID. This is the first hurdle you face when figuring out how to get a business credit card as a non-resident.

But what if you don’t have a U.S. credit history? Or what if you don’t have an SSN? That’s where the alternatives come in. Understanding how to get a business credit card really comes down to understanding these alternatives.

The Golden Ticket: What You Need Instead of an SSN

If you don’t have an SSN, you have two main paths forward when learning how to get a business credit card. One is a government-issued number, and the other is a business strategy.

Option A: Get an ITIN (Individual Taxpayer Identification Number)

This is the most common and straightforward route for individuals wondering how to get a business credit card. An ITIN is a tax processing number issued by the Internal Revenue Service (IRS) for people who have to file taxes in the U.S. but aren’t eligible for an SSN.

Think of it as a cousin to the SSN. It looks similar (it’s also a nine-digit number), and it allows the IRS to track your tax obligations. The good news? Many major credit card issuers now accept an ITIN in place of an SSN on their applications. If you are researching how to get a business credit card, getting an ITIN should be your first to-do item.

How to get one: You don’t need to visit an office. You fill out a form called a W-7 and mail it to the IRS with proof of your identity (like a passport) and your tax return. It takes a few weeks, but it’s free. Once you have this, how to get a business credit card becomes much easier.

Option B: Use Your EIN (Employer Identification Number)

This is the “business-only” route. An EIN is like a Social Security number for your business. It’s how the IRS identifies your company. When entrepreneurs ask how to get a business credit card without personal liability, the EIN is usually the answer.

Here’s the catch: Most standard business credit cards from big banks will still ask for your SSN in addition to your EIN because they want that personal guarantee. That’s just part of how to get a business credit card from a traditional lender.

However, there is a special category of cards called “EIN-only” cards. With these, you apply using only your business’s EIN and financial history. The bank looks at your business revenue, cash flow, and business credit score instead of your personal credit score. This usually means no personal guarantee is required, protecting your personal assets. If you are looking for how to get a business credit card that doesn’t touch your personal credit, this is the holy grail.

These are harder to qualify for. You generally need a strong business with solid revenue (often $100,000 to $1 million+ per year) and a few years in operation. But for established businesses, this is the best answer to how to get a business credit card without an SSN.

Top Business Credit Cards You Can Get with No SSN

Alright, let’s get to the list. I’ve broken these down into categories so you can find the one that fits your situation. Remember, how to get a business credit card often depends on matching your profile to the right issuer.

Best for Individuals with an ITIN (Traditional Cards)

If you have an ITIN, you can apply for many standard business cards. You will likely need to have some U.S. credit history, or you might start with a secured card. For most people asking how to get a business credit card, this is the most accessible path.

| Card Name | Why It’s Good | ID Needed | The Fine Print |

|---|---|---|---|

| Capital One Spark Classic for Business | Builds credit; 1% cash back; no annual fee | ITIN accepted | Requires a personal guarantee; best for fair credit |

| Bank of America Business Cards | Variety of rewards (like cash back or travel) | ITIN accepted; apply by phone or in a branch | Needs good business credit or revenue |

| American Express Business Cards | Strong rewards and sign-up bonuses | ITIN or foreign passport accepted | Annual fees often apply; requires a personal guarantee |

If you have an ITIN, how to get a business credit card is essentially the same process as for someone with an SSN—you just plug in your ITIN where asked.

Best for Businesses Using Only an EIN (Corporate Cards)

These are the “EIN-only” cards. They are typically charge cards (you must pay in full each month) and are offered by fintech companies. They look at your business’s health, not your personal credit score. If you want to know how to get a business credit card without a personal guarantee, this is your answer.

| Card Name | Best For | Key Feature | Approval Hurdle |

|---|---|---|---|

| Ramp Corporate Card | Startups and scaling businesses | Automated expense management; savings insights | Requires strong revenue (often $50k+ in bank) |

| Rippling Corporate Card | Businesses using Rippling for HR/Payroll | Integrates with HR, payroll, and IT; 1.75% cash back | Requires using the Rippling platform; revenue minimums |

| Stripe Corporate Card | Existing Stripe users | Seamless integration with Stripe payments; virtual cards | Invite-only for eligible Stripe users with transaction volume |

| BILL Divvy Corporate Card | Small to medium businesses | Flexible expense management; up to 7x points based on payment speed | May require a passport/ID check; looks at cash flow |

These companies have redefined how to get a business credit card for the modern entrepreneur. They care more about your bank balance than your personal history.

Niche Options & Fuel Cards

If you run a specific type of business, these might work for you.

- Shell Fleet Cards: If you have a fleet of vehicles, these cards focus on fuel purchases. They may check business credit rather than personal credit. Some government or non-profit entities can get them with no personal liability. This is a niche answer to how to get a business credit card for logistics companies.

- Sam’s Club Business Mastercard: You can apply for this in-store with your EIN, but it typically requires a business to be established (often 2+ years) and have significant revenue.

- Karta: This is a premium option. Karta offers a Visa Infinite card specifically for global non-residents with U.S. bank accounts. They do not require an SSN or ITIN, but you likely need significant assets. For high-net-worth individuals wondering how to get a business credit card, this is a solid option.

Step-by-Step: How to Apply

Ready to pull the trigger? Here is the game plan for how to get a business credit card when you lack an SSN.

Step 1: Get Your Paperwork in Order

You need to prove you and your business exist. This is the foundation of how to get a business credit card successfully.

- Personal ID: A valid passport is the most common document.

- Tax ID: Your ITIN letter from the IRS or your EIN confirmation letter.

- Business Docs: Articles of incorporation, business license, or a DBA (Doing Business As) certificate.

- Financials: Bank statements showing your business cash flow. For fintech cards like Ramp, they often want to see a healthy bank balance.

Step 2: Decide on Your Strategy

Your approach to how to get a business credit card depends entirely on your current situation.

- If you have an ITIN and decent credit: Go for a Capital One Spark or apply for a Bank of America card in person.

- If you have a strong business but no personal credit: Go for a fintech card like Ramp or Rippling. This is the fastest how to get a business credit card route for established businesses.

- If you have no credit history at all: You might need to start with a secured card or a “credit builder” card to establish history first. Learning how to get a business credit card sometimes means starting small.

Step 3: Apply (The Right Way)

- Online: For cards like Capital One or Amex, you can often apply online and enter your ITIN in the SSN field.

- In Person/Phone: For Bank of America and Citi, it’s often better to go into a branch or call. They can manually enter your ITIN and passport details.

- Sales Demo: For corporate cards like Rippling and Ramp, you usually have to talk to a sales rep. Be prepared to explain your business model and show your financials. This personal touch is often the secret to how to get a business credit card from fintechs.

Step 4: Start Building U.S. Credit

Once you get the card, use it responsibly. Pay on time. Keep your balances low. This activity will be reported to the business credit bureaus (like Dun & Bradstreet) and help you qualify for even better cards in the future. This final step in how to get a business credit card is the most important for long-term success.

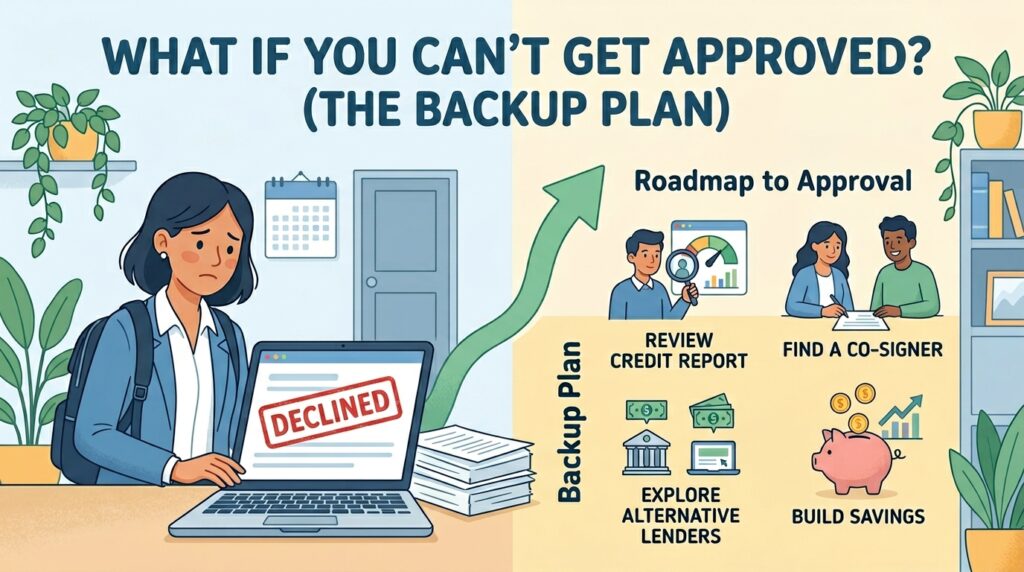

What If You Can’t Get Approved? (The Backup Plan)

Sometimes, even with the right ID, you might get denied because you have no U.S. credit history. Don’t give up. Try these methods to build a foundation. They are essential parts of how to get a business credit card when you’re starting from zero.

1. The Secured Credit Card

This is the classic “training wheels” method. You give the bank a deposit (say $500), and they give you a credit card with a $500 limit. You use it, pay it off, and build credit. For many, this is the first real step in how to get a business credit card.

- Firstcard® Secured Credit Builder Card: This one is great because it specifically welcomes international applicants with no SSN.

- Bank of America Business Advantage Unlimited Cash Rewards Secured Card: Requires a $1,000 deposit and an SSN/ITIN.

2. Become an Authorized User

Find a friend or family member in the U.S. with good credit. Ask them to add you as an “authorized user” on their personal or business card. You get a card in your name, and the positive payment history rubs off on your credit profile. Make sure the issuer reports authorized user activity to the credit bureaus. It’s a clever hack for how to get a business credit card history without applying yourself.

3. Use a Service Like Nova Credit

This is a game-changer. Nova Credit allows you to share your credit history from your home country with U.S. lenders. If you have a great credit score in the UK, India, or Mexico, some issuers (like American Express) will consider that when you apply. This is a modern answer to how to get a business credit card as a global citizen.

Common Questions (FAQs)

Q: Can I get a business credit card with just my passport?

A: Yes, sometimes. Major issuers like American Express, Citi, and Bank of America will accept a foreign passport along with an ITIN. Some fintech companies like Ramp or BILL Divvy may use a passport for identity verification, but they also need to see your business financials. So when asking how to get a business credit card, remember that a passport is just one piece of the puzzle.

Q: Do EIN-only cards require a personal guarantee?

A: Most true EIN-only corporate cards (like Ramp, Rippling, Stripe) do not require a personal guarantee. The debt is corporate liability, meaning only the business is responsible. However, to qualify, your business needs to be financially strong. This is the dream scenario for anyone researching how to get a business credit card without personal risk.

Q: I have an ITIN but no credit history. What do I do?

A: This is a common situation. You should start with a secured credit card in your own name (like Firstcard or a secured personal card) to build a U.S. credit history. After 6–12 months of on-time payments, you’ll be in a much stronger position to apply for a standard unsecured business card. This is the patient person’s guide to how to get a business credit card.

Q: Will applying for these cards hurt my credit score?

A: If you apply for a card from a major bank (like Capital One or Amex), they will do a “hard pull” on your credit report, which can temporarily lower your score. However, most EIN-only fintech cards (Ramp, Divvy) do not perform hard pulls on your personal credit because they don’t use it. They might do a “soft pull” just to verify your identity. Knowing this difference is part of smart how to get a business credit card strategy.

Conclusion: Your Business Deserves Credit

Navigating the U.S. financial system without an SSN can feel like walking through a maze blindfolded. But as you can see, the walls are starting to come down. Whether you choose to get an ITIN and apply with a traditional giant like Capital One, or you leverage your business’s cash flow to get a high-tech card from Ramp, there is a path forward for you.

Don’t let the lack of a nine-digit number stop you from building your American dream. Start by getting that ITIN or gathering your business bank statements. Pick one option from the list above, and just apply. Now that you know how to get a business credit card, the only thing left to do is take action.

The worst they can say is no. But if they say yes, you’ve just opened the door to building business credit in the United States. And that is a game-changer. Mastering how to get a business credit card is one of the smartest financial moves you can make for your company’s future.