So, you took the leap. You hung up your own shingle. You are now the CEO, the marketing department, the receptionist, and the janitor. You set your own hours, you choose your clients, and you answer to no one.

It is liberating. It is terrifying. It is the American Dream.

But then, reality hits. You are lying in bed at 2 AM, staring at the ceiling, and a cold sweat breaks out. It is not about your next deadline or a difficult client. It is about something far scarier: “What happens if I break my leg?”

For most of your life, health insurance was just a thing that happened. You filled out a form at a new job, and a card showed up in the mail. Now, the safety net is gone. You are responsible for finding and paying for your own coverage.cheap helth insurance in texas.

Welcome to the world of the self-employed. Finding affordable, reliable health insurance is often the biggest headache for freelancers, gig workers, and small business owners. But here is the good news: it is not impossible. In fact, you have more options than you think.

In this guide, I am going to walk you through every single one of them. We will look at the costs, the tax breaks, the enrollment deadlines, and the traps to avoid. By the end, you will have a clear plan to protect your health and your business.

The Big Question: Do I Really Need Health Insurance?

Let’s get this out of the way right now.

Yes. You do.

I know you are healthy. I know you haven’t seen a doctor in years. I know the monthly premium feels like a waste of money when you could use it for new software or marketing.

But health insurance is not about Tuesday. It is about the one Tuesday that changes everything.

Think about it this way. You are a freelance photographer. You are driving to a shoot, and someone runs a red light. You wake up in a hospital with a broken pelvis. You are looking at surgery, physical therapy, and months of recovery.

Without insurance, the average cost of a three-day hospital stay in the USA is around $30,000. Add surgery, and you are easily looking at $100,000 to $200,000.

That is not just a financial setback. That is bankruptcy. That is losing your house. That is the end of your business.

Matthew T., a self-employed man who shared his story on the Ramsey Solutions blog, went 20 years without insurance because he didn’t want the monthly expense. When he finally signed up, he ended up in the ER 30 days later with a serious condition. His bill came to $169,912. His new insurance saved his life and his finances.

Health insurance is not an expense. It is the shield that protects everything you are working so hard to build.

A Note on State Mandates

While the federal government no longer requires you to have health insurance, some states do. If you live in California, Massachusetts, New Jersey, Rhode Island, Vermont, or Washington D.C., you could still face a tax penalty for going without coverage . It is worth checking your local laws.

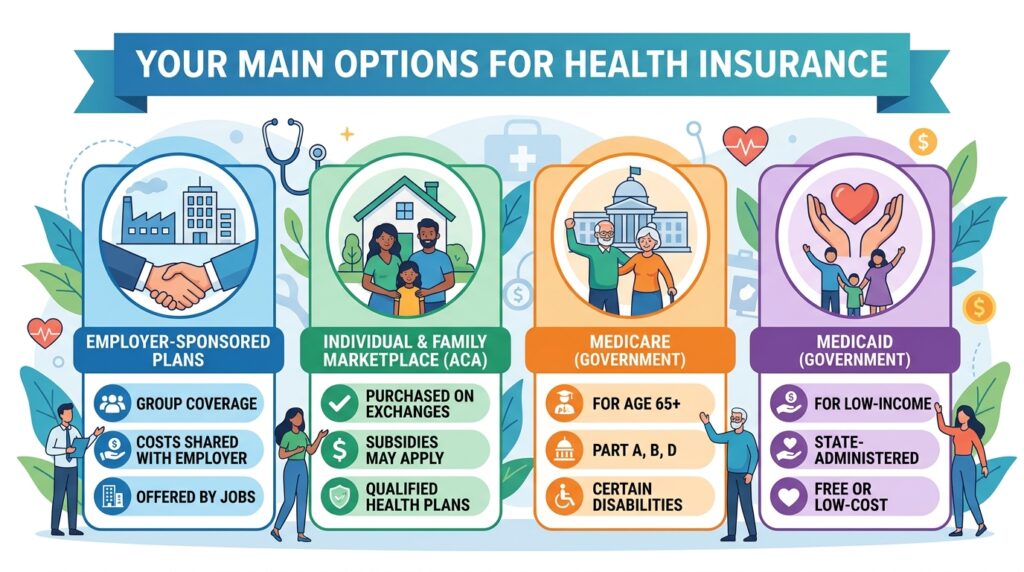

Your Main Options for Health Insurance

When you are self-employed, you have a menu of choices. Some are great for long-term security, others are just temporary band-aids. Let’s break them down.

1. The Health Insurance Marketplace (Your Best Bet)

The first place you should look is the Health Insurance Marketplace, created under the Affordable Care Act (ACA). You can access it at HealthCare.gov or through your state’s own marketplace website if you live in a state like New York, California, or Colorado .

Why the Marketplace is Great for the Self-Employed

- Comprehensive Coverage: All Marketplace plans must cover ten “Essential Health Benefits,” including emergency services, maternity care, prescription drugs, and preventive care .

- Pre-Existing Conditions: Insurers cannot deny you coverage or charge you more because you have a health issue like diabetes or asthma .

- Financial Help (Subsidies): This is the big one. If your income is between 100% and 400% of the Federal Poverty Level, you likely qualify for a premium tax credit. This credit lowers your monthly premium .

The Metal Tiers

Marketplace plans are grouped into “metal” categories. These tiers help you balance your monthly cost (premium) with your out-of-pocket costs (deductibles and copays) .

- Bronze: Lowest monthly premium, highest costs when you need care. Good for young, healthy people who only want coverage for worst-case scenarios.

- Silver: Moderate premium and moderate costs. If you qualify for “cost-sharing reductions” (which lower your deductibles), you must pick a Silver plan to get that extra help .

- Gold: Higher monthly premium, lower costs when you need care. Good if you have regular doctor visits or prescriptions.

- Platinum: Highest premium, lowest out-of-pocket costs. Best for those with significant, ongoing health needs.

2. Medicaid (Free or Low-Cost Coverage)

If your business is just starting and your income is low, you might qualify for Medicaid. This is a joint federal and state program that provides comprehensive health insurance at little to no cost .

Eligibility depends on your income and family size. In states that expanded Medicaid under the ACA, adults with income up to 138% of the Federal Poverty Level may qualify .

3. Spouse’s Employer Plan

This is often the easiest and most affordable option. If your husband, wife, or partner has a job that offers health insurance, see if you can join their plan. Because the employer usually pays a large part of the premium, this is frequently cheaper than buying your own policy .

4. COBRA (Continuation Coverage)

If you recently left a traditional job to go out on your own, you have the right to keep your old employer’s health insurance for a limited time through COBRA.

The catch? It is usually expensive. Your old employer was paying a big chunk of your premium. Under COBRA, you have to pay that full amount yourself, plus an administrative fee . You can use it as a bridge, but it is rarely a good long-term solution.

5. Professional Associations and Freelancer Unions

Some organizations offer group health insurance plans to their members. The most famous example is the Freelancers Union, which has helped connect independent workers to coverage for over 25 years .

You might also find plans through industry-specific groups, like the Graphic Artists Guild or the National Association for the Self-Employed (NASE) .

Watch Out: Before you sign up, compare the costs and coverage to a Marketplace plan. Sometimes these “group” plans are not subsidized and can be more expensive, or they may not cover all the essential benefits required by the ACA .

6. Short-Term and Catastrophic Plans (Use with Caution)

These plans are cheaper for a reason, and that reason is that they offer less protection.

- Short-Term Plans: These are designed to fill a temporary gap in coverage (a few months). They usually have lower premiums but often do not cover pre-existing conditions, mental health, or prescription drugs .

- Catastrophic Plans: Available only to people under 30 or those with a hardship exemption. They have very low premiums but extremely high deductibles. They cover you for the worst emergencies (like a car accident) and three primary care visits a year, but you will pay almost everything else out of pocket until you hit that high deductible .

My advice: Use these only if you absolutely have no other option and you understand the risks.

7. Health Care Sharing Ministries

These are not insurance. They are groups of people (often with shared religious beliefs) who pool their money to pay each other’s medical bills .

While they can be cheaper, they come with huge risks. They are not regulated by the government, they can deny coverage for things like pre-existing conditions or “unbiblical” treatments, and there is no guarantee they will pay your bill . Proceed with extreme caution.

The Golden Ticket: Tax Breaks for the Self-Employed

Here is where being your own boss pays off. The government gives you a fantastic tax break to help with the cost of health insurance.

The Self-Employed Health Insurance Deduction

If you are self-employed and have a net profit for the year, you can deduct 100% of your health insurance premiums from your taxable income .

This is an “above-the-line” deduction. That is a fancy way of saying you do not need to itemize your deductions to claim it. It directly lowers your Adjusted Gross Income (AGI), which reduces your overall tax bill .

What Premiums Are Deductible?

- Medical insurance

- Dental and vision insurance for you, your spouse, and your dependents

- Qualified long-term care insurance (up to certain limits based on your age)

- Medicare (Parts A, B, C, and D)

Bonus: You can also deduct premiums for your children under age 27, even if they are not your dependents on your tax return .

Important Rules for the Deduction

- Net Profit Required: Your business must have made a profit. You cannot claim the deduction if your business had a net loss .

- No Other Subsidized Plan: You cannot claim the deduction for any month you were eligible to participate in an employer-subsidized health plan (like through your spouse’s job) .

- Use Form 7206: To calculate the deduction correctly, you will need to use IRS Form 7206, “Self-Employed Health Insurance Deduction” .

How Much Does It Cost? (The Numbers)

Let’s talk dollars and cents. How much should you budget for health insurance?

The cost varies wildly based on your age, where you live, and the plan you choose. However, we can look at averages to give you a ballpark.

According to recent data from the Kaiser Family Foundation, the average monthly costs for Marketplace plans are roughly :

- Lowest-cost Bronze plan: Around $330 – $350 per month

- Lowest-cost Silver plan: Around $440 – $470 per month

- Lowest-cost Gold plan: Around $500 – $520 per month

But remember, these are before subsidies. If your income qualifies you for a premium tax credit, your actual monthly payment could be significantly lower.

Mastering the Timeline: When to Enroll

You cannot just buy ACA health insurance whenever you feel like it. You have to enroll during specific windows.

Open Enrollment Period (OEP)

This is the main shopping season. For coverage starting in 2026, the Open Enrollment Period for most states runs from November 1, 2025, to January 15, 2026 .

If you want your coverage to start on January 1, you usually need to enroll by December 15 .

Special Enrollment Period (SEP)

Life happens. If you miss Open Enrollment, you can still get a plan if you have a “Qualifying Life Event.” These events trigger a 60-day window (before and after the event) to sign up .

Common Qualifying Life Events include:

- Losing other health coverage (like losing your job or COBRA running out)

- Getting married or divorced

- Having a baby or adopting a child

- Permanently moving to a new area with different plan options

Frequently Asked Questions

Let’s tackle some of the most common worries self-employed people have about insurance.

I’m young and healthy. Can’t I just skip insurance and save the money?

You can, but it is a massive gamble. You are essentially betting that you will not get hit by a car, diagnosed with cancer, or need your appendix removed. As the story of Matthew T. shows, one single event can wipe out a lifetime of savings . Insurance is not for the everyday; it is for the unexpected.

How do I estimate my income for subsidies if my freelance income goes up and down?

This is a common challenge. When you apply for a Marketplace plan, you estimate your expected annual income. The subsidy is based on that estimate. If you end up making more money than you estimated, you may have to pay back some of the subsidy when you file your taxes. If you make less, you get more back . It gets reconciled on your tax return using Form 8962. Try to make your best, most honest guess.

Can I write off my health insurance premiums if my business had a loss?

Unfortunately, no. The self-employed health insurance deduction requires your business to show a net profit for the year . If you had a loss, you cannot claim the deduction on Schedule 1. However, you can still include those premium costs as part of your itemized medical expenses on Schedule A, but that only helps if you itemize and your total medical expenses exceed 7.5% of your AGI .

What is the difference between a premium and a deductible?

This is the most important thing to understand.

- Premium: The amount you pay every month, no matter what, to keep your insurance active. Think of it as your membership fee .

- Deductible: The amount you have to pay out of pocket each year before your insurance company starts paying its share for most services . If you have a $3,000 deductible, you pay for your doctor visits and prescriptions until you have spent $3,000. After that, your insurance kicks in.

What if I need to see a doctor before I meet my deductible?

You will likely pay a copay (a fixed fee, like $30) for the visit, but that money usually does not count toward your deductible. You will also be responsible for the full cost of any tests or procedures until the deductible is met, unless your plan offers specific benefits before the deductible (like preventive care, which is often free) .

Conclusion: Protect Your Dream

Being self-employed in the USA is an act of courage. You are betting on yourself. You are building something from nothing.

Do not let a preventable medical crisis be the thing that tears it all down. Navigating the world of health insurance can feel like a bureaucratic nightmare, but it is a puzzle you must solve.

Start at the Marketplace. Look at the metal tiers. See if you qualify for a subsidy that lowers your premium. Talk to an independent insurance agent if you feel overwhelmed . And remember that magical tax deduction that can lower your bill come April 15th.

Yes, it costs money. Yes, it is annoying paperwork. But in the end, health insurance for self-employed people is not just about doctor visits. It is about peace of mind. It is about knowing that you and your family are safe, no matter what life throws at you.

Now, go out there and build that empire. You have got this.