Car Insurance Explained | A Complete Beginner’s Guide 2026

So you just got your first car. Or maybe you’ve been driving for a while but still get that confused feeling whenever insurance papers show up. Trust me, I’ve been there. That stack of paperwork with all those fancy terms can make anyone’s head spin.

But here’s the thing – understanding car insurance isn’t as hard as it seems. Think of it like learning to cook a new recipe. At first, all those ingredients and steps look complicated. But once someone breaks it down for you, it starts making sense.

That’s exactly what I’m going to do today. By the time you finish reading this guide, you’ll know more about car insurance than most of your friends. And you’ll finally understand what you’re actually paying for every month.

Let’s dive in.

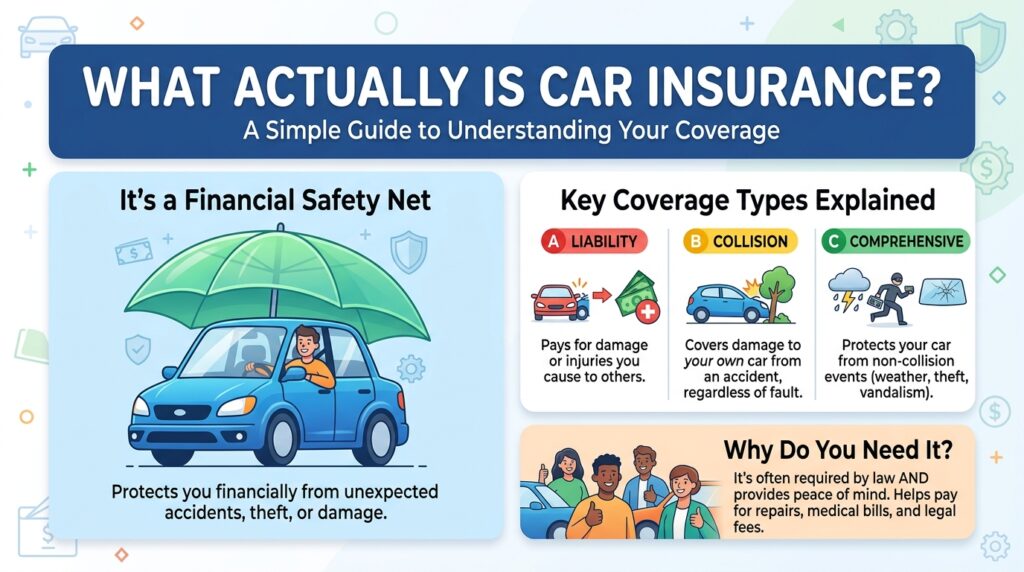

What Actually Is Car Insurance?

Car insurance explained in the simplest way possible is a promise. You pay a company a certain amount of money each month, and in return, they promise to help you out if something bad happens to your car or if you cause an accident.

Think of it like a safety net. You hope you never need it, but boy are you glad it’s there when you do Car insurance explained.

Here’s a real-life example. My neighbor Sarah backed her car into a lamppost last winter. Cold morning, sleepy eyes, and boom – big dent in her bumper. Without insurance, she would have paid around $1,200 out of her own pocket to fix it. Instead, she paid her $500 deductible, and insurance covered the rest Car insurance explained.

That’s the whole point of insurance. It turns a potentially devastating financial hit into something manageable Car insurance explained.

Why Car Insurance Isn’t Optional

You might be wondering – do I really need this? The short answer is yes. And here’s why.

First, it’s the law. Every state except New Hampshire requires you to have some form of auto insurance. Drive without it, and you’re looking at fines, license suspension, and in some cases, even jail time. Not worth the risk Car insurance explained.

Second, cars are expensive. We’re not talking about fixing a broken bicycle here. A simple fender bender can cost thousands. A serious accident? We’re talking tens of thousands or more. Most people don’t have that kind of cash lying around Car insurance explained.

Third, it protects you from other people. What if someone without insurance hits you? Or what if they have insurance but it’s not enough to cover your medical bills? The right policy has your back in these situations Car insurance explained.

The Main Types of Car Insurance Coverage

When you first look at an insurance policy, it feels like reading a foreign language. Liability, collision, comprehensive – what does it all mean? Let me break down each one in plain English Car insurance explained.

Liability Coverage

This is the foundation of every car insurance policy. Liability coverage pays for damage you cause to others. It has two parts:

Bodily injury liability pays for medical bills of people you hurt in an accident. This includes hospital stays, surgery, and even lost wages if they can’t work Car insurance explained.

Property damage liability pays for fixing things you damage. Usually that means other people’s cars, but it also covers things like fences, mailboxes, or buildings you might hit Car insurance explained.

Here’s the thing about liability – it only covers other people, not you or your car. If you cause an accident, your liability coverage helps the other driver, not yourself Car insurance explained.

Collision Coverage

This is where your own car gets some love. Collision coverage pays to repair or replace your vehicle if you hit something. That something could be another car, a tree, a guardrail, or even that giant pothole that seems to get bigger every winter Car insurance explained.

Remember Sarah and her lamppost? That’s collision coverage at work Car insurance explained.

Comprehensive Coverage

Despite the name, comprehensive doesn’t cover everything. What it does cover is damage to your car from things other than collisions Car insurance explained.

Think natural disasters, theft, vandalism, falling objects, or hitting a deer. If a hailstorm turns your car into a golf ball, comprehensive pays. If someone steals your stereo, comprehensive pays. If a tree branch falls on your hood during a storm, you guessed it – comprehensive pays Car insurance explained.

Personal Injury Protection

Sometimes called PIP, this coverage pays for medical expenses for you and your passengers, regardless of who caused the accident. It might also cover lost wages and other related costs.

Some states require this. Others don’t. But it’s worth considering even if it’s optional where you live Car insurance explained.

Uninsured/Underinsured Motorist Coverage

Here’s a scary thought – not everyone on the road has insurance. In fact, about one in eight drivers doesn’t. And plenty more carry only the bare minimum Car insurance explained.

If one of those drivers hits you, this coverage steps in. It pays for your medical bills and car repairs when the other person can’t Car insurance explained.

How Insurance Companies Decide What You Pay

Now for the million-dollar question – why does your friend pay $80 a month while you’re looking at quotes for $200? Insurance companies look at a bunch of factors to figure out your rate. Let me walk you through them Car insurance explained.

Your Driving Record

This is the big one. If you’ve had accidents or tickets in the past few years, you’ll pay more. Insurance companies see you as a higher risk. It’s like dating – past behavior often predicts future behavior Car insurance explained.

Clean record for three to five years? You’ll get much better rates Car insurance explained.

Your Age and Experience

Sorry, young drivers. Statistics show that drivers under 25 get into more accidents than older drivers. That means higher premiums. The good news is rates usually start dropping around age 25, as long as you keep your record clean Car insurance explained.

Where You Live

City drivers pay more than rural drivers. Why? More cars, more traffic, more chances for accidents. Plus, cities often have higher rates of theft and vandalism Car insurance explained.

Even your specific zip code matters. Some neighborhoods simply have more claims than others.

What You Drive

That shiny sports car might look cool, but it’ll cost you in insurance. So will luxury vehicles with expensive repair costs. On the flip side, family sedans with great safety ratings usually cost less to insure Car insurance explained.

Insurance companies look at how likely your car is to be stolen, how much it costs to repair, and how safe it is in a crash.

How Much You Drive

The more time you spend on the road, the higher your chances of an accident. If you have a short commute or work from home, you might qualify for lower rates. Long-haul truckers and daily commuters pay more Car insurance explained.

Your Credit Score

This one surprises a lot of people. In most states, insurance companies can use your credit history to help set your rates. Studies show a connection between credit and the likelihood of filing claims Car insurance explained.

Better credit usually means lower insurance premiums.

Making Sense of Deductibles

You’ll hear the word “deductible” a lot when shopping for insurance. It’s simple – your deductible is what you pay before insurance kicks in Car insurance explained.

Let’s say you have a $500 deductible and damage that costs $3,000 to fix. You pay $500, your insurance pays $2,500.

Higher deductibles mean lower monthly payments. Lower deductibles mean higher monthly payments but less out of pocket when something happens Car insurance explained.

There’s no right answer here. It depends on your savings and your comfort with risk. Can you afford a $1,000 hit if something happens? Then a higher deductible might save you money over time. Would that break the bank? Stick with a lower deductible.

How Much Coverage Do You Really Need?

This is where a lot of people get confused. You want to be protected, but you don’t want to pay for coverage you don’t need. Here’s some practical advice Car insurance explained.

State Minimums Usually Aren’t Enough

Every state sets minimum coverage requirements. And almost always, those minimums are too low. Way too low.

Say your state requires $25,000 in bodily injury coverage. That sounds like a lot until you realize a single day in the hospital can cost more than that. If you cause a serious accident, you could be on the hook for anything beyond your coverage limit Car insurance explained.

A good rule of thumb is to carry enough coverage to protect your assets. If you own a home or have savings, you want enough insurance to cover what you could lose in a lawsuit Car insurance explained.

Consider Your Car’s Value

Here’s a simple way to think about collision and comprehensive. If your car is worth less than $3,000-$4,000, these coverages might not make financial sense. Why pay $500 a year to protect a car that’s only worth $2,000?

But if you have a newer car or one you’re still making payments on, you’ll want both collision and comprehensive. Your lender will require them anyway.

Think About Your Health Insurance

If you have good health insurance, you might not need as much medical coverage through your auto policy. But remember, health insurance won’t cover your passengers. And it won’t help with deductibles or co-pays related to the accident.

Money-Saving Tips That Actually Work

Who doesn’t want to save money on car insurance? Here are strategies that really make a difference.

Bundle Your Policies

Most insurance companies will give you a discount if you buy multiple policies from them. Home and auto is the most common combo. Renters and auto works too. Ask about bundling – it could save you 10-25%.

Shop Around Every Year

Here’s something insurance companies don’t want you to know – loyalty doesn’t always pay. Rates change. Your situation changes. Other companies might offer better deals to win your business.

I shop my insurance every year or two. Sometimes I stay with the same company. Sometimes I switch. But I always know I’m getting a fair price.

Ask About Discounts

Insurance companies have dozens of discounts, but they won’t always tell you about them. You have to ask.

Common discounts include:

- Good driver discounts

- Good student discounts

- Multi-car discounts

- Safety feature discounts (anti-lock brakes, airbags, anti-theft devices)

- Defensive driving course discounts

- Low mileage discounts

- Pay-in-full discounts

Raise Your Deductible

Remember what we said about deductibles? Raising yours from $500 to $1,000 could lower your premium by 15-30%. Just make sure you have that $1,000 saved up in case you need it.

Maintain Good Credit

Since credit affects your rates in most states, keeping your credit score healthy can save you money on insurance. Pay bills on time, keep credit card balances low, and only apply for credit when you really need it.

Common Car Insurance Myths Debunked

There’s so much misinformation about car insurance out there. Let me clear up a few things.

Myth: Red Cars Cost More to Insure

I hear this one all the time. It’s completely false. Insurance companies don’t care what color your car is. They care about the make, model, engine size, and safety features. Paint color doesn’t affect risk or repair costs.

Myth: Insurance Follows the Driver, Not the Car

This one gets people in trouble. Generally, insurance follows the car. If you lend your car to a friend and they crash it, your insurance pays – not theirs. There are exceptions, but that’s how it usually works.

Myth: Minimum Coverage Is Good Enough

We talked about this earlier. Minimum coverage might save you money today, but it could cost you everything tomorrow. One serious accident can wipe you out financially if you’re underinsured.

Myth: Your Credit Doesn’t Matter

As we discussed, in most states it absolutely does. Insurance companies have data showing that people with better credit file fewer claims. So they use credit as one factor in setting rates.

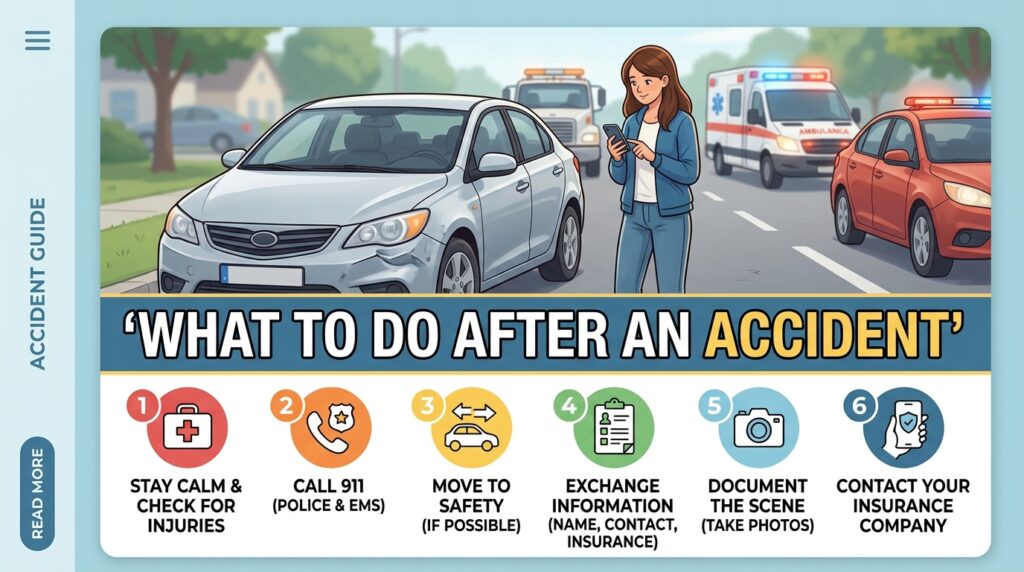

What to Do After an Accident

Nobody plans to have an accident, but they happen. Knowing what to do ahead of time makes a stressful situation much easier to handle.

Step 1: Check for Injuries

First things first – is anyone hurt? If so, call 911 immediately. Your health and the health of others comes before anything else.

Step 2: Move to Safety

If the cars are drivable and it’s safe, move them out of traffic. If not, turn on your hazard lights and stay in the car with your seatbelt on until help arrives.

Step 3: Call the Police

Even for minor accidents, it’s good to have an official report. Police can help manage traffic and document what happened. If it’s a minor fender bender in a parking lot, they might not come, but it’s worth calling to find out.

Step 4: Exchange Information

Get the other driver’s:

- Name and contact information

- Insurance company and policy number

- Driver’s license number

- License plate number

- Car make and model

Step 5: Document Everything

Take pictures. Lots of them. Get shots of both cars from multiple angles. Get close-ups of the damage. If there are skid marks or debris in the road, photograph those too. If anyone witnessed the accident, get their contact information.

Step 6: Notify Your Insurance

Call your insurance company as soon as possible – ideally from the scene or within a few hours. They’ll walk you through the next steps. Be honest about what happened, but stick to the facts. Don’t guess or speculate about who was at fault.

Understanding Your Policy Documents

Insurance policies aren’t exactly beach reading. But you should understand the basics of what’s in yours.

Declarations Page

This is the summary. It shows:

- Your name and address

- The cars covered

- The types and amounts of coverage

- Your deductibles

- Your premium and when it’s due

- Discounts applied

Think of it as the cheat sheet for your policy.

Insuring Agreement

This section explains what your insurance company promises to do. It outlines the coverages you bought and the situations where they apply.

Exclusions

Equally important – this tells you what’s NOT covered. Common exclusions include intentional damage, racing, using your car for business (unless you have special coverage), and driving without permission.

Conditions

This part covers the rules. How to file a claim, what to do if you’re sued, how to cancel your policy – stuff like that.

When to Review Your Coverage

Your insurance needs change over time. Here are moments when you should take a fresh look at your policy.

You Pay Off Your Car

Once you own your car outright, you might adjust your coverage. You’re no longer required to carry collision and comprehensive, though you might still want them.

You Move

Moving to a new zip code can change your rates. Always update your insurance when you move.

You Get Married

Married people often pay less for insurance than single people. Congratulations – now call your agent.

A Teenager Starts Driving

Adding a young driver increases your rates, but there are discounts available. Good student discounts, driver’s ed discounts, and more.

Your Life Changes

Got a promotion? Bought a house? Started working from home? All these things can affect your insurance needs and rates.

Frequently Asked Questions

Q: Can I drive someone else’s car with my insurance?

A: Generally yes, but it depends. Your insurance usually follows you when you drive someone else’s car with their permission. But their insurance is typically primary, meaning it pays first. Check your policy for details.

Q: What happens if I let my insurance lapse?

A: Nothing good. You’ll likely face higher rates when you get coverage again. In some states, you might face fines or license suspension. Plus, you’re driving uninsured, which is risky and illegal.

Q: Does insurance cover rental cars?

A: Sometimes. Many policies include rental reimbursement if your car is being repaired from a covered claim. But that’s different from coverage when you rent a car for vacation. Check your policy or call your agent before you rent.

Q: How long does an accident affect my rates?

A: Usually three to five years, depending on your state and insurance company. After that, it typically falls off your record for rating purposes.

Q: Can I cancel my policy anytime?

A: Yes, but there might be fees. And if you’re canceling because you found a better deal, make sure your new policy starts before the old one ends. You don’t want a gap in coverage.

Q: Does insurance cover theft of personal items from my car?

A: Usually not. Your car insurance covers damage to the car itself. Items stolen from your car – like a laptop or golf clubs – are typically covered by your renters or homeowners insurance.

Q: What’s the difference between stated value and actual cash value?

A: Actual cash value pays what your car is worth today, accounting for depreciation. Stated value lets you declare how much your car is worth, but you might not get that full amount if it’s totalled. For classic or exotic cars, you might want agreed value coverage.

Making Your Final Decision

By now, you know way more about car insurance explained than when you started reading. You understand the coverages, the costs, and the common pitfalls. So how do you actually pick a policy?

Start by getting quotes from at least three companies. You can do this online or through an independent agent who can quote multiple carriers at once.

Compare more than just the price. Look at:

- Coverage limits – are they similar?

- Deductibles – are they the same?

- Discounts – did each company apply everything you qualify for?

- Company reputation – check reviews and financial strength ratings

Don’t be afraid to ask questions. A good insurance agent will be happy to explain things until they make sense. If they rush you or make you feel stupid, find someone else.

Remember, the cheapest policy isn’t always the best. You want coverage that will actually be there when you need it. That means a company that pays claims fairly and has the financial strength to do so.

A Few Final Thoughts

Car insurance isn’t the most exciting topic, I know. But understanding it gives you power – the power to make smart choices, save money, and protect yourself from financial disaster.

Think of it this way. You spend hours researching which car to buy. You compare features, read reviews, test drive different models. Your insurance protects that investment and your financial future. It deserves at least a little of your time and attention.

The good news is you don’t have to be an expert. You just need to understand the basics, know what questions to ask, and review your coverage now and then to make sure it still fits your life.

Car insurance explained really comes down to one simple idea – it’s peace of mind. Peace of mind that if something happens, you won’t face it alone. Peace of mind that your savings are safe. Peace of mind that you can get back on the road and back to your life.

Drive safe out there. And if you ever have questions about your coverage, you know where to find answers now.